Following futures positions of non-commercials are as of December 6, 2016.

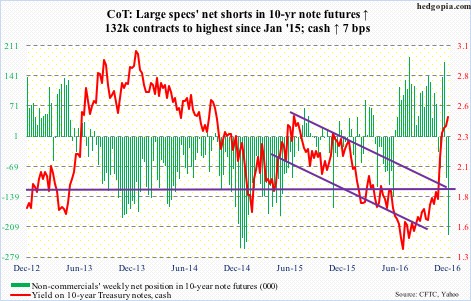

10-year note: Regardless how Mr. Mario Draghi, ECB president, describes the €20-billion/month reduction in asset purchases beginning next March until December, it looks like tapering, walks like tapering, and talks like tapering.

The good thing for Mr. Draghi was that major Eurozone stock markets did not freak out on Thursday. But yields rose, which the euro responded to by rallying initially but was sold hard in the end. Talk about confused traders!

The bigger message in all this is this – the ECB is reaching the end of its stimulus rope. As of November, its balance sheet stood at €3.6 trillion, up from €2 trillion in September 2014. By next December, this would have swollen to €4.3 trillion, which equates to two-fifths of the Eurozone GDP. Is it any wonder they feel the need to begin to taper?

Currently net short 228.6k, up 132.3k.

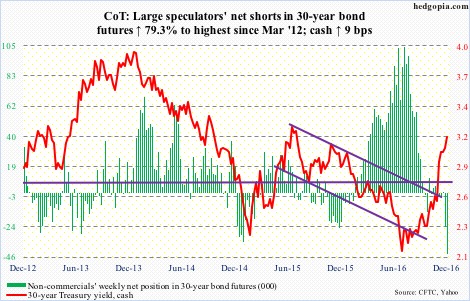

30-year bond: Major economic releases next week are as follows.

FOMC meeting begins on Tuesday, and ends the next day. Post-meeting, a press conference is scheduled. Markets expect a hike, and will be more interested in language/hints in regards to potential tightening path for next year.

Also on Tuesday comes out the NFIB small business optimism index for November. October was up eight-tenths of a point month-over-month to 94.9. The cycle high 100.3 was reached in December 2014.

Wednesday brings PPI-FD (November), retail sales (November), and industrial production (November).

Producer prices were unchanged m/m in October, and increased 0.8 percent in the 12 months through October. Core PPI edged down 0.1 percent m/m, but rose 1.6 percent in the 12 months through October.

Retail sales in October rose 0.8 percent m/m to a seasonally adjusted annual rate of $465.9 billion. Sales grew at a two-year high 4.3 percent year-over-year.

Industrial production declined 0.9 percent y/y in October. This was the 14th straight y/y contraction. Capacity utilization fell 1.2 percent y/y to 75.3 percent – the 20th straight y/y decline. Utilization reached a cycle high 78.9 percent in November 2014.

CPI (November), the NAHB housing market index (December), and Treasury International Capital (October) are due out on Thursday.

Consumer prices rose 0.4 percent m/m in October; y/y, they increased 1.6 percent. Core CPI only managed a 0.1-percent rise m/m, while y/y it advanced 2.1 percent. This was the 12th straight y/y increase of north of two percent.

Builder sentiment was unchanged in November at 63. September was 65, matching the reading in October last year – a 10-year high.

On a 12-month running total basis, foreigners continue to sell U.S. equities, but at a decelerating pace. In September, this stood at minus $55 billion, down from an all-time high of minus $138.9 billion in February this year.

Housing starts for November are scheduled for Friday. October shot up 25.5 percent m/m to 1.32 million units (SAAR). This was the highest since August 2007.

Currently net short 43.6k, up 19.3k.

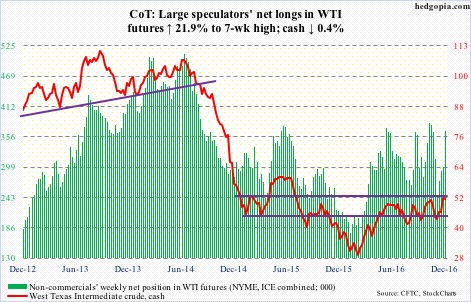

Crude oil: Last week, spot West Texas Intermediate crude jumped 12.2 percent, ending right at the neckline of a reverse-head-and-shoulders formation, which, if fulfills, can be bullish. This week, crude rallied to $52.42 on Monday to unsuccessfully break out of that resistance at $52-ish.

Daily indicators are itching to move lower. The week produced a doji. Oil bulls expended too much energy last week. There is support at $49. The 50-day moving average lies at $48.37.

The weekly EIA report was not of much help either.

In the week ended last Friday, U.S. gasoline and distillate stocks rose – by 3.4 million barrels to 229.5 million barrels and by 2.5 million barrels to 156.7 million barrels, respectively – to 14- and eight-week highs, in that order.

Crude imports jumped 755,000 barrels per day to 8.3 million b/d.

The good thing is, refinery utilization inched up six-tenths of a point to 90.4 percent. Similarly, crude stocks dropped by 2.4 million barrels to 485.8 million barrels – a four-week low. Last but not the least, crude production inched down 2,000 b/d to 8.7 mb/d.

Currently net long 366.2k, up 65.8k.

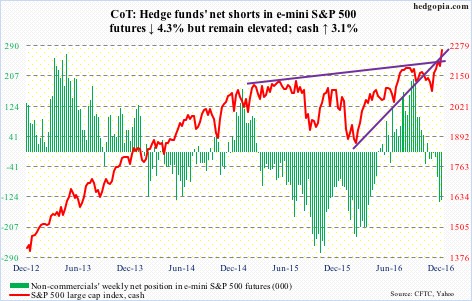

E-mini S&P 500: Yet another week, and yet another all-time high. The Trump rally marches on. Wednesday’s 1.3-percent jump took out the previous high 2214.1 of five sessions ago. Bulls would now be looking to defend this the next time the cash weakens. In the last two sessions last week, they were able to defend three-month support at 2190-ish.

There is giddiness in the air.

Both the Dow Industrials and Transports rallied to new all-time highs. For proponents of the Dow Theory, this is a buy signal. Whatever that means. On a trailing 12-month basis, the S&P 500 is trading at north of 22x operating earnings – so let us not even talk about valuation support.

That said, momentum is intact, and the crowd has decided the U.S. election has changed the risk-reward dynamics. In the latest week, Investors Intelligence bulls were 58.8 percent – the highest since February last year. The NAAIM (National Association of Active Investment Managers) exposure index was at 101.6. The chips have been pushed to the middle of the table. All good so long as another party is willing to pay a higher price (the greater fool theory).

The risk in all this is that nouveau investors will be left holding the bag when the music stocks. Traders tend to be flexible and hopefully will dodge the bullet.

In the week ended Wednesday, $4.5 billion moved into SPY, the SPDR S&P 500 ETF. In the prior couple of weeks, $3.4 billion was redeemed (courtesy of ETF.com).

Also in the week through Wednesday, $2 billion came out of U.S.-based equity funds (courtesy of Lipper).

Currently net short 133.3k, down 6k.

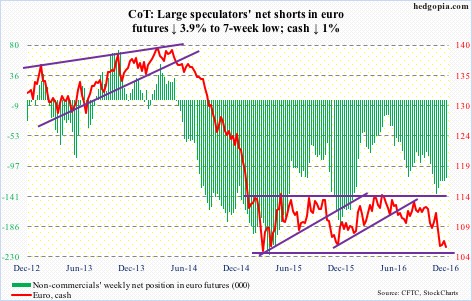

Euro: In the wake of Sunday’s Italian referendum decision, the cash dropped to a 21-month low overnight before recuperating. In regular trading on Monday, it jumped 0.9 percent to 107.97, but was rejected at gap-down resistance of mid-November.

Come Thursday, in a whipsaw session, markets interpreted the ECB decision as euro bearish, slamming it down 1.3-percent, and then by another 0.5 percent on Friday. The November 23 low of 105.25 needs to hold.

Currently net short 114.6k, down 4.7k.

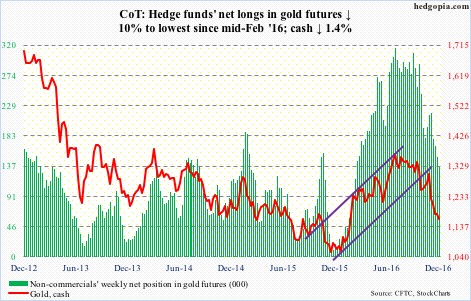

Gold: The cash is trying hard to stabilize, and is at a good spot for gold bugs to put their foot down. At $1,172.3, gold would retrace 61.8 percent of the November 30 (2015)-July 5 (2016) rally.

But flows continue to disappoint. In the week ended Wednesday, GLD, the SPDR gold ETF, lost another $751 million. This followed outflows of $2.8 billion in the prior three (courtesy of ETF.com).

Currently net long 136.4k, down 15.2k.

Nasdaq 100 index (mini): The saga continues. Even as the S&P 500, Russell 2000 and Nasdaq composite rallied to fresh highs this week and a Dow Theory buy signal was flashed, the Nasdaq 100 refuses to join the party. Sort of. It still has not posted a new high. The last one was on October 25 (4911.76).

That said, it did rally 3.3 percent this week – past its 50-day moving average, and past resistance at 4840.

The problem continues to be flows. In the week ended Wednesday, QQQ, the PowerShares Nasdaq 100 ETF, lost $2.6 billion (courtesy of ETF.com). Since Mr. Trump was elected president, $885 million has been redeemed.

Currently net long 52.7k, down 36.5k.

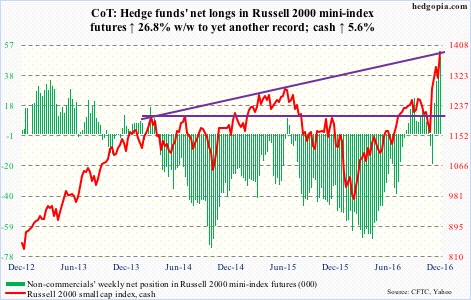

Russell 2000 mini-index: From post-Thanksgiving Friday to Thursday last week, the cash declined 2.8 percent. Turns out that was a pause to refresh. From that low, it then rallied six-plus percent. Wednesday’s low successfully tested the post-Thanksgiving high. In other words, buyers are showing up where they are supposed to – technically speaking.

It has all come down to technicals right now. In a late-cycle economy, there is no fundamental basis for an index to surge 20 percent in a month – north of 16 percent post-Trump win – which is what the Russell 2000 has done.

On this basis, as overbought as the cash is, momentum is yet to break, although flows are beginning to weaken.

In the week ended Wednesday, IWM, the iShares Russell 2000 ETF, lost $327 million. This came on the heels of inflows of $5.3 billion in the prior three (courtesy of ETF.com).

That said, non-commercials accumulated net longs to yet another record. Plus, IWM short interest jumped 6.2 percent in the November 16-30 period to a 14-month high, and these shorts probably got squeezed.

Currently net long 49.4k, up 10.4k.

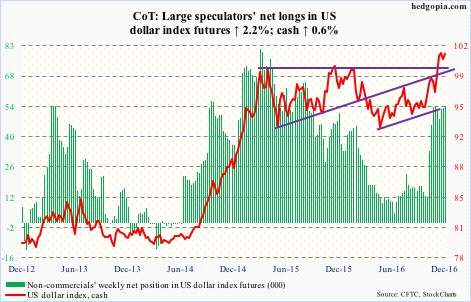

US Dollar Index: Dollar bulls obviously expended lots of energy in rallying the cash past 100. Since May this year, it jumped 11 percent, and in the process has priced in a lot – from stronger economic growth to higher interest rates.

This has pushed weekly momentum indicators into gross overbought zone. All along, non-commercials never seriously jumped on the rally bandwagon.

In the right circumstances, there is a lot of unwinding left in the cash. Near-term, it is itching to have another go at the November 25 high of 101.97.

Currently net long 54.6k, up 1.2k.

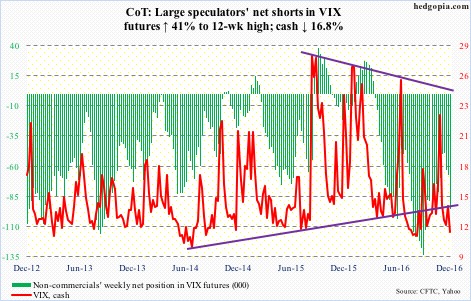

VIX: Intra-day Wednesday, the cash dropped to 11.33. This was the second straight sub-12 reading. But by close, it rallied to 12.22, up 3.7 percent. The S&P 500 jumped 1.3 percent in that session. Quite a divergence. This was also a session in which the CBOE put-to-call ratio dropped to a complacent 0.46, matching the low of June last year.

Thursday saw the same phenomenon, with the spot dropping to 11.3 intra-day but closing up 3.4 percent to 12.64, the S&P 500 rallying 0.2 percent and the P2C ratio at 0.5. Come Friday, VIX dropped seven percent to close at 11.75, with the P2C ratio at 0.53.

At Wednesday’s lows, the VIX-to-VXV ratio dropped to 0.75, before rising a tad. By the end of the week, it stood at 0.77 – well into oversold territory, and a fourth straight week in that zone.

The rubber band is stretched.

Currently net short 95.4k, up 27.7k.